Login

Login

Product Know-how

Discount certificates

Discount certificates make it possible for you to buy an underlying instrument for less than its current market price. However, the maximum payback on a discount certificate is limited to a predetermined amount (cap). The lower the cap, the greater the discount.

Discount certificates normally have a term to maturity of one to three years. At maturity, a determination is made of where the price of the underlying instrument stands. If it is at or above the cap, you’ll earn the maximum return and receive payment of the amount reflected by the cap.

If the price of the underlying stock is below the cap on the maturity date, the corresponding number of shares is usually delivered into your account. For discount certificates based on indices, baskets, currencies or fixed income securities, you’ll receive instead a cash settlement reflecting the value of the underlying instrument as it stood on the maturity date. However, in certain instances, cash settlement can also be arranged for discount certificates on shares.

If you hold your discount certificate through to maturity, you’ll only incur a loss if the price of the underlying instrument has fallen so far that the discount has been totally eroded. In essence, the discount works like a cushion against price declines in the underlying instrument. If you in fact incur a loss with a discount certificate, it will in any case be less than the amount you would have lost by investing directly in the underlying instrument.

Discount certificates work particularly well in sideways markets. If you expect that to be the case, it’s best to choose a product with a cap that’s relatively close to the current price of the underlying instrument. Products with a cap somewhat above the current price are suitable if you anticipate modestly rising markets.

Extremely defensive discount certificates with a cap far below the current market price of the underlying instrument (deep-discount certificates) are also used by some investors as a substitute for time deposits. With this approach, you can achieve annual returns of three to five per cent while enjoying a relatively comfortable safety buffer.

Endless discounts

The classical version of a discount certificate as described above has evolved in recent years with issuers creating an array of interesting byproducts. One of them is the «rolling discount certificate». This product type is no longer constrained by a predetermined maturity date…it just keeps on rolling. Your capital is continually reinvested at regular intervals – in most cases either once a month or once a quarter – in new synthetic discount certificates.

Because normal discount certificates often tend to gain the greatest amount of value in the final weeks of their term, you as an investor gain optimum benefit with these short-running, artificial discounts from sideways moves in the market, and this without your having to constantly swap in and out of certificates. There’s a catch of course: in a heartbeat, a short, sharp downside move in the market can eradicate all of the many small gains you’ve booked over time with your rolling discount certificate.

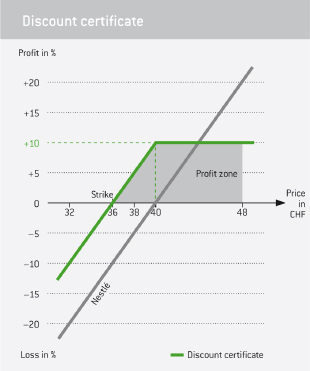

Example of a discount certificate

| Remaining term to maturity : | 1 year |

| Underlying : | Nestlé |

| Maximum payout: | CHF 40.00 |

| Current price of certificate: | CHF 36.00 |

| Current price of stock: | CHF 40.00 |

If at maturity of the certificate after one year’s time Nestlé is trading above the cap of CHF 40, you’ll be paid out the maximum amount of CHF 40 for each certificate you own. Thus in this example, a sideways movement in the stock already suffices for you to earn the maximum return of 11.1 percent. If the stock falls below the cap, for example by 5 percent to a level of CHF 38, your account will be credited with one Nestlé share for each certificate you own. Nevertheless, you still earned a modest profit of about 5.5 percent because the certificate was initially purchased at CHF 36. Only if the shares decline by more than 10 percent and upon maturity of the certificate stand at a level below CHF 36 would you incur a loss - assuming of course that you immediately sell the shares you receive at that lower price.